-01.png)

CHF WEEKLY ROUND-UP: January 22-26, 2024

- Adam Komet

- Jan 26, 2024

- 6 min read

Updated: Apr 3, 2024

Canadian Markets leveled off this week after failing to break out to new all-time highs as it appeared would happen in the first week of the new year. The TSX composite is building a base near 21,000, positioning itself to challenge the all-time high of March 2022, only 100 points away.

The Bank of Canada held its policy rate steady for a fourth consecutive meeting on Wednesday and explicitly stated for the first time that it won’t need to increase it again if the economy evolves in line with its forecasts. Rate cuts are generally expected to begin in April, but it may be unrealistic to expect rate cuts in the first half of the year unless recession sets in. Canada has been dancing with a technical recession for over a year, only avoiding it because of adjusted GDP numbers and high population growth. The Federal Government’s use of high levels of immigration to prop up GDP seems to have run its course, as detailed in a report by National Bank Financial that calls it a “Population Trap”. (special-report_240115.pdf (nbc.ca)). Inflationary wage increases are continuing, especially in the public sector.

U.S. equity markets dipped slightly on Thursday after rising five straight days. Today, it appears to be moving further into all-time high territory, continuing to be driven by Big Tech. The S&P 500 went over 4900, and the NASDAQ Composite hit 15,629. The 10-year Treasury yield rose to just under 4.15% while the 2-year yield ticked down to just under 4.4%. The US Dollar index has strengthened so far this year DXY in the 103’s.

The Fed will be meeting next week. Rate changes are not expected, but rate cuts could be fewer and later than expected by the markets. The US GDP increased at a 3.3 percent annualized rate, according to the government’s preliminary estimate out Thursday. For the year, the US economy grew at an annualized rate of 2.5%, up from 1.9% in 2022. A closely watched measure of underlying inflation rose two percent for a second straight quarter, in line with the Federal Reserve’s target, the Bureau of Economic Analysis report showed. Could the soft landing have already happened?

A U.S. presidential election year shows a seasonal pattern that is classically a good time for stocks. This may not be significant in the short term but will likely play a larger role in market activity closer to the polling date. Currently, the election looks more and more like a contest between two 80+-year-old men from the two political extremes, neither of whom is truly suitable to serve.

The gold market remains well supported above the $ 2,000/oz level, where it has built some good support, but is slow to attract bullish momentum, while interest rates remain high. Silver is clinging to support at $23/oz. with no signs of the hoped-for breakout. Don’t avoid precious metals, ferocious action can come at any time.

Base metals have started to show some strength this week, Copper at $ 3.85/lb is up over 3% this week. Nickel, Lead, and Zinc are also showing small moves on the upside. Korean battery manufacturer Samsung made a major investment in Canada Nickel of $18.5 million to own 8.7 percent of the company. Money seems to be moving to the sector, watch for other moves.

Most mining investors plan to maintain or expand their positions in the sector in 2024 as they seek to draw a line under disappointing returns last year, according to Mining Journal Intelligence’s (MJI) Investor Sentiment Report 2024.

Battery materials remained weak; a slight uptick was seen in Lithium, but at $13.47/kg, it is still less than 20% of the price of a year ago. Cobalt remained flat at $ 13.22/lb, the pandemic lows. EV growth has not materialized outside of China and US carmakers have excess unsold inventory. Ford and GM have cut back production, and even Tesla has suggested sales growth will be lower than forecasted. Sayona Mining is conducting an operations review of its North American Lithium (NAL) operation in Quebec, the only operating hard rock lithium mine in North America, in order to “optimize the cost structure to manage cash flow and enhance financial sustainability during a bear market for lithium”. An additional fourteen staff were laid off. The project is a joint venture of Sayona (75%) and Piedmont Lithium (25%). Australian operator Liontown Resources on Monday indicated that it may delay the planned ramp-up and expansion of its flagship Kathleen Valley lithium project following a decline in prices. Perhaps a washout of the Lithium sector is occurring, and favorable investments will be revealed by the end of the year; stand by.

Oil prices have risen to $ 76.80/bbl (WTI) as tensions in the Red Sea continue, combined with a surprise drop in US inventories of 9.2 million barrels last week, where a decline of 2.2 million was expected. US production had dropped to a 5-month low, removing a million barrels/day of production.

Uranium held the gains of last week and remains at $ 106.00/lb the highest since August 2007. The Government of Niger’s decision to temporarily suspend the granting of new mining licenses and review existing ones marks a significant move towards overhauling its mining sector but is creating insecurity of supply in the short term. Interest in Uranium, the cornerstone of the nuclear power industry, has grown along with global efforts to foster clean energy, leading to stronger demand for the heavy metal for nuclear power plants. Shares of the uranium miners and exchange-traded funds have some catching up to do.

It has been a quiet week for our clients. We’re happy to present to you our round-up of news released between January 22-26, 2024.

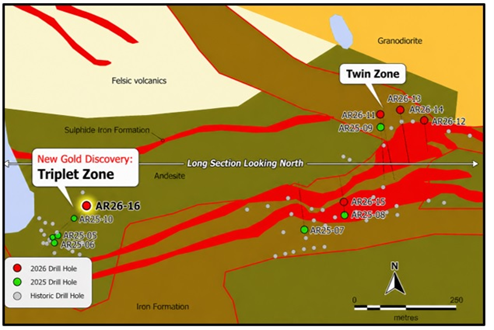

On January 23, 2024, Sokoman Minerals Corp. (TSXV: SIC) (OTCQB: SICNF) announced an update on the ongoing exploration at the flagship Moosehead Gold Project. Since November 28, an additional 6 holes (890 meters) have been completed 400 m to the east of the Eastern Trend, with five intersecting the recently discovered 552 Zone and the 6th collaring in an extensive fault zone (believed to be the Cape Ray – Valentine Lake shear zone), which was terminated after cutting 75 m of intensely deformed volcanic and intrusive units.

The 552 Zone is extremely significant as it represents an entirely new gold-bearing structure on the Moosehead property, with signs of potentially high-grade mineralization as three of the five most recent holes displayed visible gold within 50 m of surface. Of significance, is the presence of mineralized float located near the 552 Zone that returned 10.3 g/t Au that is believed to be derived from the 552 Zone. The 552 Zone is 400 m to the east of the main Eastern Trend, and it remains open. The closest mineralization is at the 253 Zone located 150 m north of 552, which is poorly understood and requires additional drilling, and which may represent a parallel zone. Drilling planned to test the down-plunge extent of the 552 Zone in 2024 should also intersect any parallel structures, including extensions to the 253 Zone where previous drilling returned 1.56 g/t Au over 1.60 m. Phase 6 drilling completed to date now sits at 101,519 m including 20,519 m in 70 holes in 2023. A proposed 2,500 m winter program will commence in about two to three weeks and will focus on the 552 Zone where we are starting to see improved grades and some visible gold.MH-23-574 featuring 552 Zone veining – 5.00 g/t Au over 2.10 m (64.55-66.65 m)

Drilling has defined a continuous, two to five-metre wide, zone of quartz veining/quartz breccia, in variably to undeformed sedimentary units. Three holes intersected white quartz veins with specks of visible gold (MH-23-572, 574 and 575). The quartz veining is locally vuggy (epizonal type), located in a west-northwest trending, 50-to-70-degree northeast dipping structure. The veins carry trace to 5% sulphide minerals including boulangerite, sphalerite, chalcopyrite, pyrite and arsenopyrite, the mineral assemblage common to most gold zones on the property.

Drill hole MH-23-557 intersected the zone, giving 1.04 g/t Au over 3.65 metres.Table 1 – Assay Results

Have a great weekend,

Cathy Hume, CEO

ALLOW CHF TO WORK FOR YOU!CHF Capital Markets is Canada’s longest-established capital markets and investor relations firm, serving an international portfolio of NASDAQ, TSX, TSX Venture, and CNSX-listed companies across all sectors and market cap sizes.

Our team consists of high-profile communications and investment industry specialists who provide individually crafted solutions for clients operating in a broad range of industries providing comprehensive representation to the investment community as a separate, complete, and comprehensive outsourced IR department.

CHF’s reputable IR services include:Provide prompt and credible information to existing shareholdersOutreach continuously to expand shareholder and financial community interestManage financial community expectations so that actual performance can exceed the anticipatedManage the mechanics of IR service seamlessly so that Management’s time is not wasted on routine

tasksManage social media presence

Let us get your story heard!

For more information please contact:

Cathy Hume, CEO

T: +1-416-868-1079 x 251

Comments